IRS Form 7004 gives businesses an automatic 6-month extension to file their tax return. It is a short, two-part form — but filing it incorrectly, or misunderstanding what it covers, can lead to costly penalties.

IMPORTANT: Form 7004 extends your filing deadline only — not your payment deadline. Any taxes owed are still due on the original due date. Interest and late-payment penalties apply to any unpaid balance regardless of whether you filed the extension.

Who Can File Form 7004?

Form 7004 is available to business entities, including:

- C corporations

- S corporations

- Partnerships

- Multi-member LLCs (taxed as partnerships or corporations)

- Certain trusts and estates

- REITs and regulated investment companies

Sole proprietors who report business income on Schedule C with their personal Form 1040 use Form 4868 instead — not Form 7004.

Form 7004 must be filed on or before the original return due date — not after. The extension itself is not retroactive.

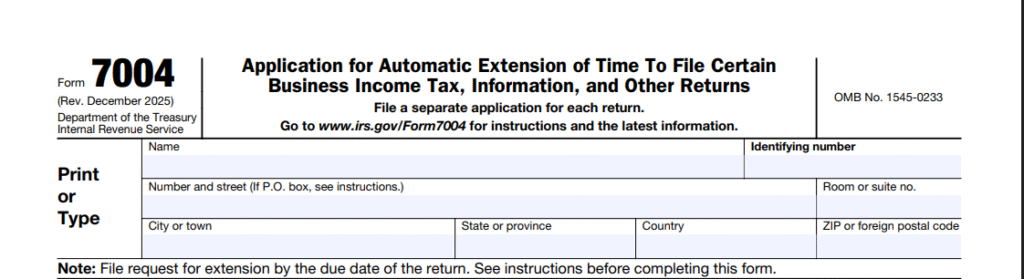

How to Complete Form 7004 – Line-by-Line Instructions

Form 7004 has two parts and eight lines.

Before you begin, gather your EIN, legal business name (exactly as it appears in IRS records), tax period dates, estimated total tax liability, and all payments made to date.

Note: A name mismatch between the form and IRS records is a leading cause of rejection. You cannot file Form 7004 without a valid EIN — if your EIN application is pending, wait until it is assigned.

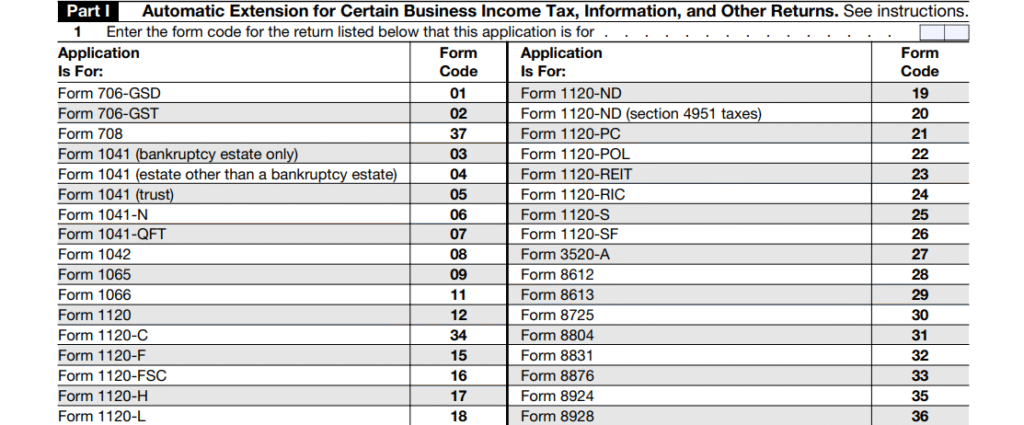

Part I — Line 1: Form Code

Enter the two-digit code for the return you are extending. This is not the form number itself — it is a separate code listed in the IRS instructions. Using the wrong code is the most common reason for rejection.

| Code | Form | Description |

|---|---|---|

| 09 | 1065 | Partnership income |

| 12 | 1120 | C Corporation income |

| 25 | 1120-S | S Corporation income |

| 04 | 1041 | Estate or Trust income |

| 06 | 1042 | Annual withholding — U.S. source income of foreign persons |

| 15 | 1120-F | Foreign corporation income |

The full code list is in the official IRS Form 7004 instructions. Always verify before filing.

2025 Update: Form 708 has been added to the list of returns eligible for extension via Form 7004. Form 708 reports tax on covered gifts or bequests received from covered expatriates under IRC Section 2801. Note that Form 708 must be filed on paper — e-filing is not available for this form.

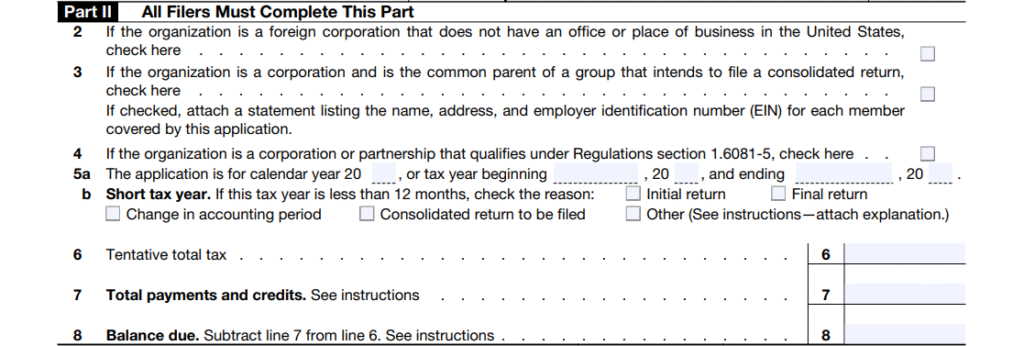

Part II — Lines 2–8: Filer Information

Line 2 — Office Outside the U.S.

Check this box if your business maintains an office or principal place of business outside the United States. This applies to foreign corporations without a U.S. office and domestic corporations conducting business and keeping records abroad.

Line 3 — Consolidated Group Return

Check if you are the common parent or agent filing a consolidated return on behalf of a corporate group. You must attach a statement listing the name, address, and EIN of each member of the group.

Line 4 — Regulation 1.6081-5

Check if your entity qualifies for an automatic extension under IRS Regulation Section 1.6081-5. Qualifying entities include partnerships and corporations keeping records outside the U.S. and Puerto Rico, foreign corporations with a U.S. office, and U.S. citizens or residents with a tax home outside the U.S. The extended deadline under this provision is the 15th day of the sixth month following the close of the tax year.

Line 5a — Tax Year Dates

If your business uses a fiscal year (not a calendar year ending December 31), enter the beginning and ending dates of your tax period. Calendar-year filers leave this blank.

Line 5b — Short Tax Year

Check the applicable reason if the period covered is less than 12 months. Common reasons include an initial return (first year of business), final return (business ceasing operations), or a change in accounting period. If the short year results from a change in accounting period, IRS approval is generally required — see Form 1128 for details.

Line 6 — Tentative Total Tax

Enter your best estimate of total tax liability for the year. This field is required — do not leave it blank. Review last year’s liability and adjust for known changes in income, expenses, or credits. Include income tax, alternative minimum tax, and any other taxes due with the return. Do not subtract nonrefundable credits here, but do subtract refundable credits.

Tip: It is better to slightly overestimate. Overpayments generate a refund when you file your actual return. Underestimates trigger penalties and interest on the shortfall.

Line 7 — Total Payments and Refundable Credits

Enter the total of all payments already made for the year: estimated tax payments, withholding, overpayments from the prior year applied to the current year, and refundable credits.

Line 8 — Balance Due

Subtract Line 7 from Line 6. This amount must be paid by the original deadline — not the extended deadline. Form 7004 only extends the time to file, not the time to pay. Failure to pay the balance due on time results in a late-payment penalty of 0.5% per month (up to 25%) plus daily compounding interest.

The 90% Rule: The IRS will not impose a late-payment penalty if you pay at least 90% of your total tax liability by the original deadline and pay the remaining balance when you file your return. This is the IRS safe harbor for estimated payments.

How to File

E-Filing (Recommended)

E-filing provides near-instant confirmation, built-in error checking, and the ability to pay any balance due in the same transaction. The IRS requires many corporations to e-file. Use an IRS-authorized e-file provider or software to submit Form 7004 electronically.

2025 Note: Forms 8924 and 8928 must also be filed on paper — e-filing is not available for these forms. (Form 708 paper-only requirement is noted at Line 1 above.)

Paper Filing

If filing by mail, use certified mail with return receipt as proof of timely filing. The correct IRS mailing address depends on your entity type, state of business, and total assets. Always verify the address in the official IRS Form 7004 instructions before mailing, as addresses vary by form type.

State Extensions

A federal Form 7004 extension does not automatically extend your state return in most states. California, New York, Illinois, Massachusetts, and Pennsylvania all require a separate state extension form filed by the same deadline as the federal return. Check your state’s Department of Revenue for specific requirements. Failure to file a state extension separately can result in state-level late filing penalties even if your federal extension is accepted.

Frequently Asked Questions

No. Form 7004 does not require a signature. If e-filing, submission through an IRS-authorized provider serves as authentication. If mailing, simply complete and send the form.

Yes, for most entity types. Many IRS-authorized e-file providers offer Form 7004 e-filing at no cost. However, Forms 708, 8924, and 8928 must be filed on paper for the 2025 tax year.

If your electronic submission is rejected, the IRS provides a perfection period of 5 calendar days to correct the error and re-transmit. The most common rejection causes are a name control mismatch (the business name does not match IRS records) and an incorrect form code on Line 1. Fix the specific error noted in your rejection notice and resubmit immediately.

No. Form 7004 provides only one automatic extension. No further extensions are available after the 6-month period.

Yes, you still need to file. Your final return is due by the 15th day of the 3rd month after the date of dissolution. If you cannot meet that short-year deadline, file Form 7004 and check the Short Tax Year box on Line 5b, noting the reason as “Final Return.”

You cannot file Form 7004 without a valid EIN. Do not leave the EIN field blank or substitute a Social Security Number. Wait until your EIN is assigned. If the deadline is approaching, call the IRS Business & Specialty Tax Line to expedite.

– Entering the form number instead of the two-digit form code on Line 1

– Leaving Line 6 (tentative total tax) blank

– Assuming the extension also extends the payment deadline

– Assuming the federal extension covers state tax obligations

– Missing the original deadline — the extension must be filed on or before that date

– Name or EIN mismatch with IRS records, causing rejection

– Underestimating the tax on Line 6, triggering underpayment penalties